Agricultural input prices remain 'historically high'

The rate of inflation in prices paid for goods and services has eased since peaking in the autumn, according to the Agriculture and Horticulture Development Board (AHDB).

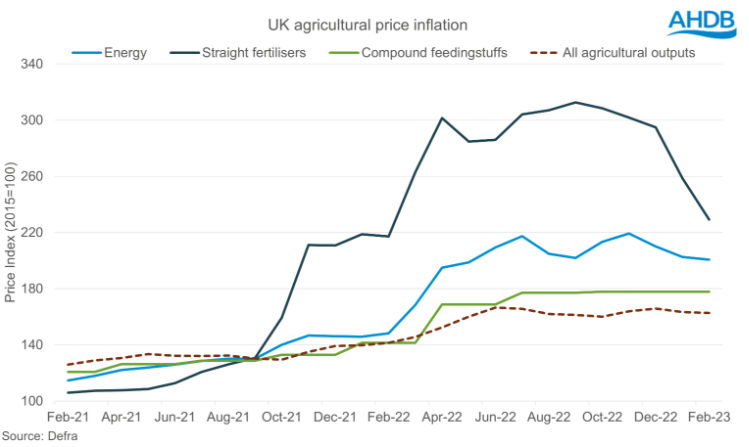

However price inflation continues to sit at "historically high" levels with key inputs maintaining a higher rate of inflation than outputs the latest Agricultural Price Index (API) shows.

The API reflects the change in the price farmers have paid for goods and services in relation to the base year of 2015.

The index highlights that fertiliser price inflation has fallen by the greatest level - 22% in the first 2 months of the year (Dec22 vs Feb23) and is down 27% compared to the inflationary peak in September

But price inflation is still up 6% compared to February 2022 and sits at an exceptional 116% above the level from two years ago.

Freya Shuttleworth, senior analyst (dairy and livestock) for AHDB, said it anticipates fertiliser price inflation to continue to ease in the short term as it follows the same trajectory of the natural gas market.

According to Shuttleworth energy price inflation has also eased, but at a "much slower rate".

It is down just 4% from the start of the year and has seen a 9% drop compared to November, when inflation peaked as winter energy demand picked up. However year-on-year, energy price inflation has increased by 35%.

Shuttleworth said:

"We would expect to see inflation to continue to ease as we leave the winter demand period, however with a cooler and wetter spring this year it is likely that energy demand has remained higher for longer."

She has advised farming businesses to look into UK government support schemes in relation to energy prices.

This includes the Energy Bills Discount Scheme, which runs until March 31 of next year, features a higher level discount for those who qualify as part of the energy and trade intensive industries, which includes dairy, meat and fish processors.

According to the latest API Inflation for compound feeds has remained flat since peaking in the summer but is now sitting at 26% above the level it was this time last year and 47% above the level seen in 2021.

Shuttleworth said:

"Wheat futures markets are currently at a similar price point to February last year, before the Russian invasion of Ukraine.

"While short term volatility in grain markets is likely with the Black Sea Initiative nearing renewal, longer term fundamentals point to a less pressured price outlook, with ample global grain supply expected for next season."