Irish cattle prices ease despite ‘continued supply constraints’ – ADHB

Irish prime cattle prices have come under pressure in the early part of this year, despite supplies remaining well below last year's levels, according to the Agriculture and Horticulture Development Board (ADHB) in the UK.

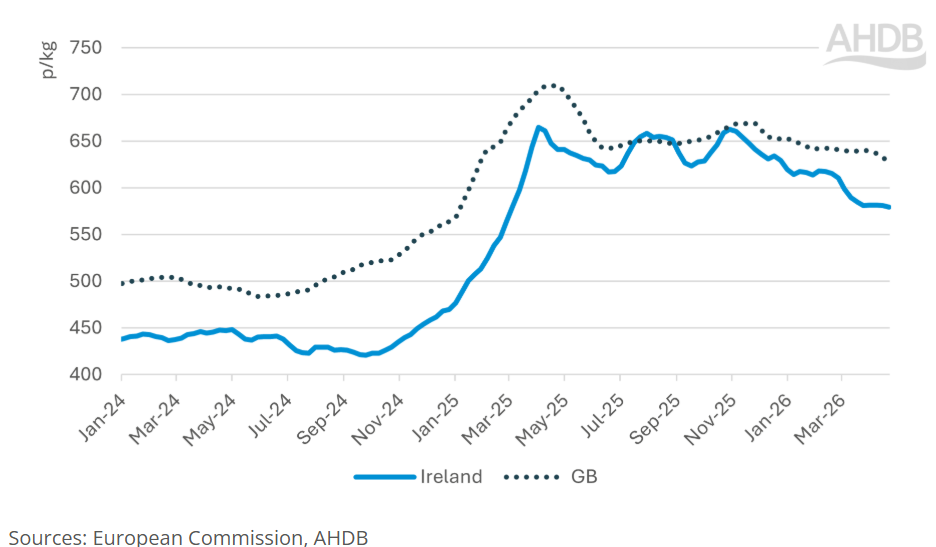

It said: “Irish prime cattle prices have steadied in recent weeks, following a period of declines in the spring. Steers averaged 581p/kg in the week beginning April 20.

“Values fell for seven consecutive weeks through February and March, as reports suggested demand for cattle wavered and stocks backed up on farm.”

However, ADHB found that “prices appear to have stabilised in recent weeks, with buying demand for cattle lifting”.

According to the body, “commentary suggests that improved weather has boosted demand somewhat, particularly for steaking cuts”.

It added: “With Irish prices falling at a steeper rate than those in GB, we have seen the differential widen, to 47p/kg in the latest week’s data (week beginning April 27).

“This wider price differential is likely impacting trade volumes across the Irish Sea.”

The figure above shows weekly R3 deadweight steer prices for GB (dark blue dotted line) and Ireland (light blue solid line) in sterling terms. GB prices generally track above Irish.

Cow prices

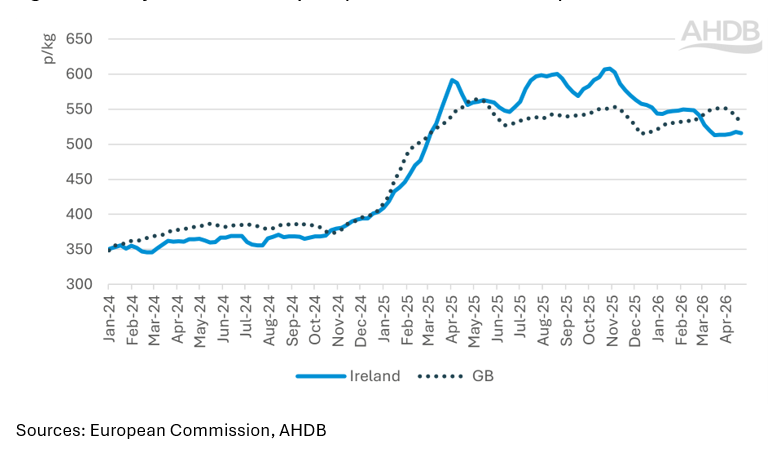

ADHB found that cow prices “track more closely across the two markets generally but have shown more volatility in recent months”.

It said: “Irish prices moved significantly above the GB market through 2025 on the back of significantly reduced kills but have recently moved closer to a more typical price position in relation to GB levels.

“Irish cows were at a near 13p/kg equivalent discount to GB in the week beginning April 27 (average across 'O3' cow carcases).

“Irish cow slaughter so far in 2026 has been lower year-on-year (-19% for 18 weeks to April 27), and weekly throughputs have been in a similar range to those recorded in the second half of 2025.”

The graph above shows weekly 'O3' deadweight cow prices for GB (dark blue dotted line) and Ireland (light blue solid line). The prices historically track closely together, however have experienced more volatility in recent months.

Supply

ADHB reported that, in the year to date, “Irish cattle kill (excluding calves) has totalled 552,300 head (18 weeks to April 27), back 13% on the same period of 2025”.

It said: “Fewer numbers were seen across all categories, with the largest fall seen in cow numbers.

“Tightness in supply has characterised the European beef market over the last eighteen months and Ireland is no exception to this trend.

“Forecasts for 2026 suggest that this is likely to continue, with the European Commission expecting a 2.6% annual decline in beef production in 2026.”

Imports

ADHB said that in the first two months of the year, imports of fresh and frozen beef into Ireland “totalled 6,800t, growth of nearly 70% versus the same period a year ago”.

The organisation added: “Monthly volumes were at a similar level to those recorded at the end of 2025, following growth through the year.

“The UK is the majority supplier into the Irish market at over 90% market share and has driven this increase.”

“This likely reflects the closeness in price between the two markets during the period, incentivising greater movement of beef across the Irish Sea.”

It added that, with the price differential widening in recent weeks, “the effect on trade volumes will be a key watchpoint as the year progresses”.

Exports

ADHB found that export volumes “have also been impacted by both the price differential and supply dynamics outlined above”.

It added: “In the period Jan-Feb 2026, fresh and frozen beef exports from Ireland totalled 54,600 tonnes, a fall of 13% compared to 2025.

“Volumes declined to almost all key markets, including the UK, France and the Netherlands.

“Indeed, subdued demand (hampered by beef price inflation) in the UK and EU markets will be having an impact.”

ADHB added that live exports “also form a key part of Irish beef trade, particularly into the EU”.

It said: “Supply constraints are evident in performance so far this year, with Bord Bia reporting that total live exports are down 18% year-on-year (year to April 25).

“Reductions were seen in all categories, with steepest falls across finished (-35%), stores (-26%), and weanlings (-30%).”

It added that calves make up the largest proportion of live exports, with numbers down by 14% year-on-year.

Buying activity

ADHB reports that Irish beef prices “appear to have steadied in recent weeks”, with reports suggesting “increased buying activity as we move towards a key beef demand period in May and June”.

It added that supplies are forecast to remain tight, which would point to an “underlying level of support for farmgate prices generally moving forwards”.

It said: “Export prospects may improve as the year progresses, as Irish prices now sit more competitively compared to both GB and others on the continent. This improved positioning may help to stimulate demand further along the supply chain.”

However, it went on to add that “longer-term impacts of price inflation across critical UK and EU markets remain a key risk for consumer purchasing and overall beef demand”.

“Competition from other suppliers into the EU and UK markets remain a watchpoint for Irish trade, especially with constrained Irish production prospects.”