Top NI dairy advisor calls for move to milk solids based pricing

One of Northern Ireland's most respected agricultural advisors has called for the region's dairy industry to make the move to a solids-based pricing structure in a bid to better incentivise farmers to improve their milk quality.

In a special guest column for AgriLand, Jason McMinn of FarmGate Consultancy reflects on how the costs of milk production compare with milk pricing over what has been a difficult year for the industry. He writes:

This year (2019) has been a difficult year for many dairy farmers in NI. Our average clients’ break-even milk price (27.8p) is above the actual milk price this year (around 27p).

Many of the costs (wages, contracting, workers pensions) will not come down again, and other costs are ticking upwards all the time (for example, drugs, hardware, vaccines etc.).

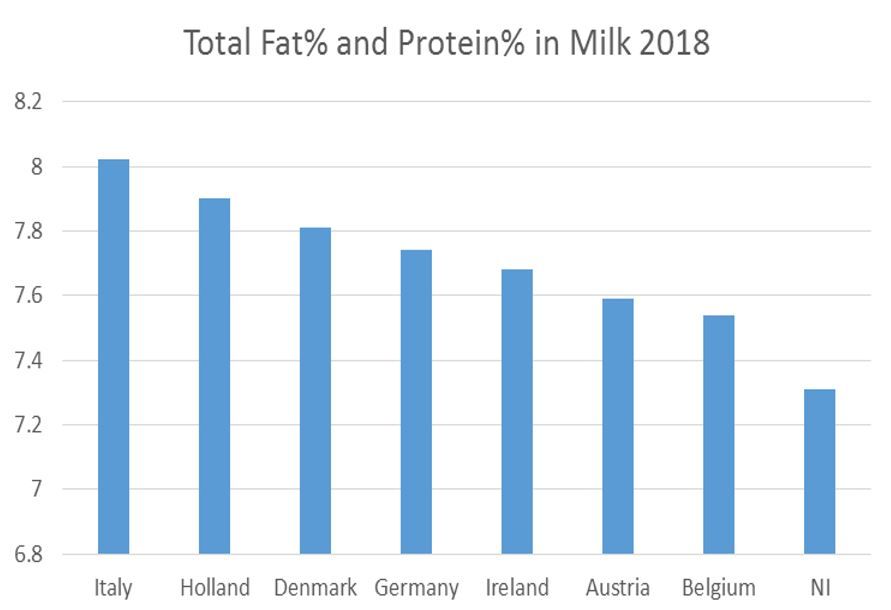

With so much talk about milk prices and pricing, I looked into our average fat and protein and milk prices compared to other European areas. Graph 1 (below) shows that we are well behind in terms of milk solids % constituents.

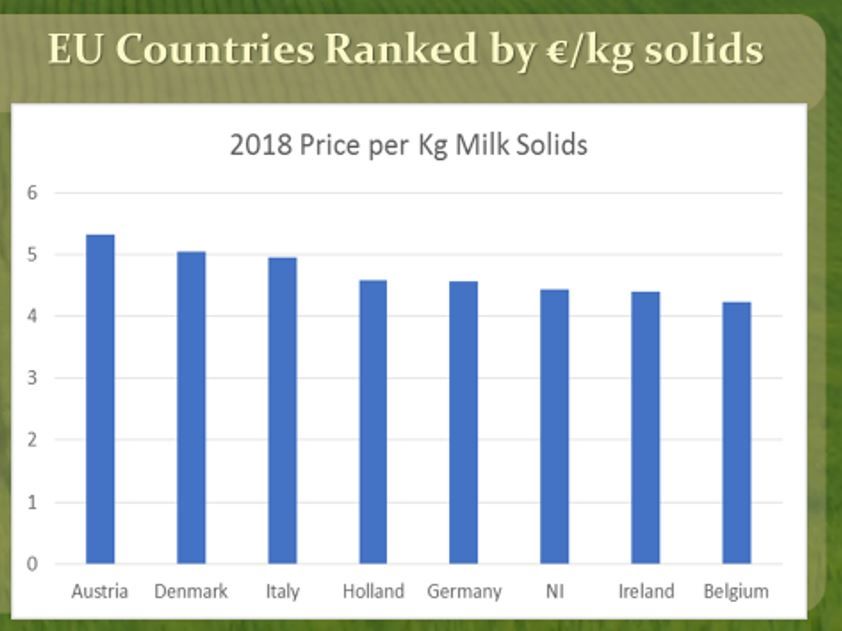

When we look at this graph we can see that our processors are paying fairly competitively for milk on a per kg solids basis, as we were slightly ahead of ROI and Belgium in 2018, and just behind Holland and Germany.

Milk solids are what we export in the form of powder, butter and cheese, not litres.

Our problem is that we have been concentrating for the last generation on producing more litres, and we now find ourselves as an industry taking a milk price which is below the break-even point of 27.8p/L (all costs, drawings, tax and bank/hp payments included).

Costs are rising all the time, and many dairy farmers have no further room for expansion.

The implications that this has for milk processors in NI is that their suppliers are on structurally lower prices than other regions in Europe. Over time this leaves our local dairy industry less competitive, which is worrying. This should cause concern amongst our milk processors.

This is why I, and others, have been calling for a change to solids-based pricing. The new payments may not be A+B-C, but the price increments for Fat and Protein need to be market-linked, and not based on an old model which was devised when milk price was 18p-20p on average.

Give our farmers the signal to produce higher milk solids and they will respond. In the South, they have increased from 3.83% fat and 3.33% protein to 4.1% fat and 3.58% protein in 10 years.

This is the way to add value to our milk pool as an industry. Marginal litres has been the strategy for many years, but with feed price/kg being so close to the milk price/L (known as the feed price to milk price ratio), it is doubtful whether marginal litres are delivering extra profit at current base prices.

Source Eurostat