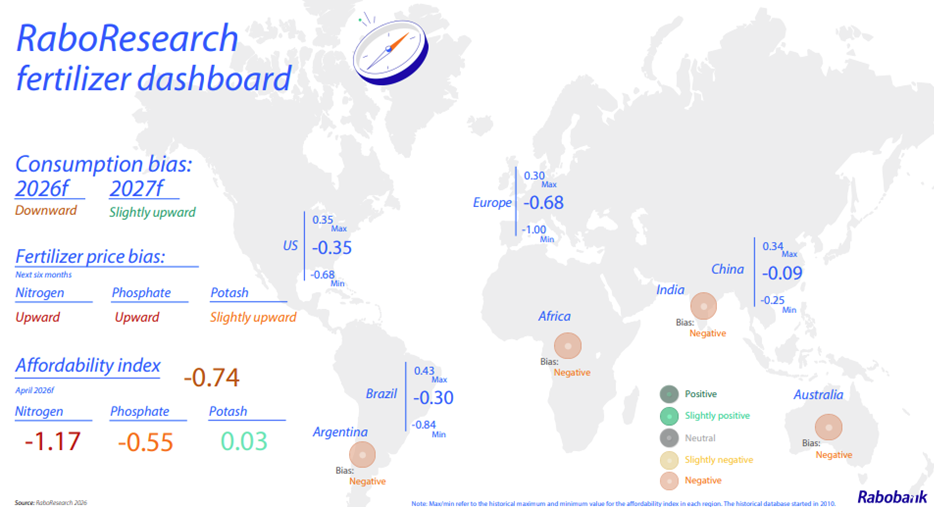

Global fertiliser outlook – how countries are weathering the crisis

There will be “continued pressure” and “increased risks” on farmers around the world as a result of the fertiliser crisis, according to a Rabobank outlook for 2026.

The Semi-Annual Global Fertiliser Outlook shared that geopolitical disruption in the Middle East and the closure of the Strait of Hormuz have removed a “substantial volume of fertilisers and critical inputs from global trade, triggering an abrupt supply shock that cannot be quickly replaced”.

Prices for nitrogen and phosphates have risen faster than agricultural commodity prices, compressing farm margins, and “accelerating affordability stress”.

The outlook for 2026 points to “continued pressure on farm economics and increased risks for global crop production and food price stability”.

Europe

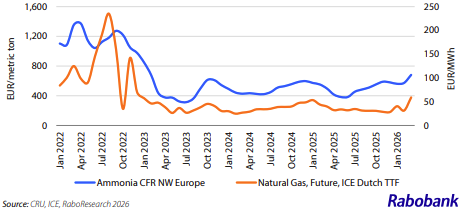

Even though Europe sources limited volumes from the Persian Gulf, farmers have seen urea prices climb around 40% since the conflict began, in line with global increases of nearly 50% from pre-conflict levels, the report said.

Nitrogen fertiliser prices were already more than 20% above 2025 levels at the start of this year, with further increases of 15-20% since the war, while ammonia has risen by 12%.

Algeria and Egypt remain the EU’s primary supplier of urea and ammonia, but both face risks around gas availability and potential production curtailments.

Russia has re-entered the European market despite higher EU tariffs, though export capacity remains constrained by operational issues, including drone strikes and a suspension of ammonium nitrate exports.

EU policymakers are proposing a temporary suspension of most-favoured-nation (MFN) duties on key nitrogen fertilisers for all countries except Russia and Belarus – though analysts expect this to have a limited impact on supply.

Meanwhile, the EU’s Carbon Border Adjustment Mechanism (CBAM) remains in force, requiring importers to account for embedded carbon emissions, alongside rising transport and insurance costs.

Australia

For Australian farmers, margin pressure remains a key concern, with the country heavily relying on imports for urea and MAP.

Rabobank estimates Middle East granular urea prices have surged 57% year-to-date, to around AUD$915 per metric tonne (MT).

The Australian dollar, traditionally a “key shock absorber for imported inputs”, has strengthened sharply over the past 12 months, the report said

The AUD/USD conversion is up nearly 12% year-on-year to around USD$0.70, its highest level since early 2023.

Despite this currency appreciation, fertiliser import prices remain elevated, sustaining fears of retail price inflation.

Africa

The conflict has highlighted how important Africa’s fertiliser producers have become to global supply.

Egypt and Algeria have become critical nitrogen exporters, with urea prices rising from $480/MT in February to around $800/MT.

Nigeria is strengthening its position in Brazil and the US, supported by its three urea plants with a combined capacity of over 3.3 million metric tonnes of ammonia and 3.2 million metric tonnes of urea.

Morocco holds considerable pricing power in the global phosphate market, with dose area product (DAP) values climbing above $800MT in March.

Zambia has expanded domestic blending and production capacity more than sixfold, moving toward near self-sufficiency.

Ghana has shifted from a subsidy scheme to free fertiliser distribution for the 2026 season.

To prevent a recurrence of past crises, a continent-wide response mechanism has been announced, emphasising “rapid decision-making and synchronised regional action” to keep fertiliser trade secure.

Brazil

Brazil imports roughly 90% of all fertiliser used in the country.

Last year, 36% of urea imports were sourced from the Middle East, down from 53% in 2021.

About 70% of Brazil’s urea imports arrive between May and December, meaning timing can benefit importers – but only in the context of short-term disruptions, which does not seem to be the current case, according to the Rabobank report.

From early January to March 19, urea prices at Brazilian ports increased by approximately 76%.

Rabobank forecasts fertiliser demand will drop from 49 million metric tonnes in 2025 to around 47.5 million metric tonnes in 2026.

China

China’s exposure is relatively limited, as it is largely self-sufficient in phosphate and nitrogen fertilisers.

Although China remains a significant importer of potash, its suppliers – Russia, Belarus, Canada and Laos – do not rely on transit through the Strait of Hormuz.

Therefore, China’s potash supply chains are largely insulated from geopolitical disruptions in the Middle East.

However, sulphur, a key input for phosphate fertilisers, remains China’s main vulnerability, due to high import dependence and sensitivity to disruption.

Chinese authorities have imposed strict phosphate export restrictions from mid-March till the end of August, to insulate the market from global price volatility.

South Asia

Some of the biggest consequences of the Iranian war may yet unfold in India, Pakistan, and Bangladesh.

Energy rationing has reduced domestic fertiliser production to about 70% capacity in some areas.

Pakistan also relies on Qatar to supply roughly 99% of its liquified natural gas (LNG) demand.

India imports between 5-6.5 million metric tonnes of DAP annually, with increased reliance on Saudi Arabian supplies, as China reduced its supply to the global market.

“Many risks are on the horizon for this region,” Rabobank warned.

The US has committed to emergency deliveries to India – a sign, Rabobank says, of just how tight global markets have become.

India produces between 40-45% of domestic DAP consumption, which requires around 2 million metric tonnes of sulphur imports.

With around 48% of global sulphur exports trapped behind the Strait of Hormuz, sulphur prices are going in the wrong direction amid tight supply, the report said.

US and Canada

Rising around 70% since the start of the year, wholesale urea prices have added as much as $35/ac to the cost of producing maize in the US.

Timing has been a mitigating factor in the US as many decisions were made before the February 28 conflict.

The US imports around 5 million metric tonnes of urea annually, with about 20% coming from Qatar, volumes of which are now caught up in the disruption.

Despite the US’ greater self-reliance in Urea Ammonium Nitrate (UAN) and anhydrous ammonia, the urea spike has pushed these prices up by 20% and 10% respectively.

With no clear mechanism in place to reduce prices, Rabobank warned that affordability will remain a key issue for farmers well into 2027.