Yara sees 41% year-on-year jump in Q1 earnings despite global fertiliser shock

Fertiliser producer Yara has recorded a 41% year-on-year increase in operating profit for the first quarter (Q1) of 2026

The Norwegian company today (Friday, April 24) released its financial results for Q1 2026, which showed its earnings before interest, tax, depreciation and amortisation (EBITDA), excluding special items, was $896 million.

This reflects a 41% increase from the same quarter a year ago, driven by “higher volume deliveries, enhanced margins across segments, and continued strong performance on improvement initiatives and disciplined cost control,” Yara stated.

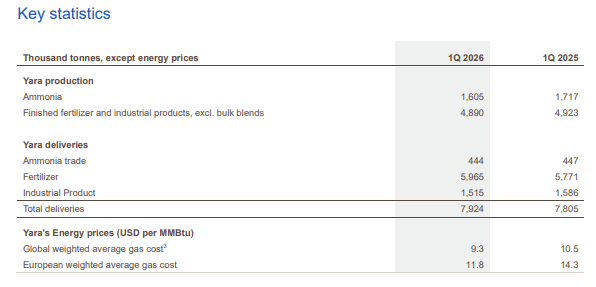

Total deliveries were 2% higher than for the same quarter a year ago mainly from increased deliveries of Amidas (urea), three-component fertilisers containing nitrogen (N), phosphorus (P), and potassium (K) or NPKs, and Calcium Nitrate (CN) fertilisers.

Yara’s president and chief executive officer, Svein Tore Holsether, said: “The quarter delivered strong results, reflecting increased nitrogen margins, solid volumes and a sustained focus on operational performance.”

He added that developments in the Middle East put “significant pressure on the global food system, with knock on effects across the value chain and growing challenges for farmer affordability”.

“The volatility highlights how fragile the food system is, and why resilient fertiliser supply chains and a strong farming community are essential.

“Fertilisers play a critical role in food security, and Yara remains focused on upholding production and deliveries.

“By utilising its global business model, Yara is well positioned to optimise operations in an uncertain global environment marked by increased regional price and demand volatility,” Holsether said.

Performance

According to the Q1 report, Yara’s revenue and other income rose to $4.2 billion, compared with $3.6 billion in the same quarter last year.

Net income reached $326 million, up from $294 million in Q1 2025.

Its operating income recorded was $610 million, almost double its figure in Q1 2025 of $308 million.

Basic earnings per share increased to $1.28 from $1.15.

Return on invested capital doubled from 6.0% in 2025 to 12.2% in 2026.

Total product deliveries reached 7.9 million tonnes in Q1 2026, up 2% year-on-year, from 7.8 million tonnes in the same quarter last year.

Yara reported that crop nutrition volumes were led by:

- 2.1 million tonnes of NPK;

- 1.3 million tonnes of urea;

- 1.2 million tonnes of nitrates.

Global results

In Europe, Yara’s EBITDA in Q1 2026 excluding special items was $246 million for the region, 54% higher than for the same quarter a year ago.

Yara stated the improvement was driven by “higher fertiliser prices, stronger margins, and continued lower fixed cost base”.

For the Americas, EBITDA for Q1 2026 excluding special items was $229 million, 48% higher than for the same quarter a year ago, “mainly reflecting increased deliveries, better nitrogen upgrading margins, and continued solid commercial performance,” according to Yara.

In Africa and Asia, EBITDA excluding special items for Q1 2026 was $44 million, 33% lower than for the same quarter a year ago, Yara said this was due to “continued margin pressure in key Asian markets, partly offset by improved product mix effects.”

In terms of global production EBITDA excluding special items for Q1 2026 was $173 million, 51% higher than for the same quarter a year ago, with Yara stating this mainly reflects “higher upgrading margins.”

Production outputs were 9% below the same quarter last year following “unplanned ammonia outages.”

Resilience

At the January 2026 Capital Markets Day, Yara introduced the next phase of its improvement programme, which targets an “incremental $200 million EBITDA improvement by the end of 2027 and a further $150 million EBITDA improvement by the end of 2030”.

These improvements will be achieved through “enhanced asset utilisation, logistical optimisation, targeted market opportunities and disciplined capital reallocation”.

Yara said: “Diversifying energy exposure and optimising the business to mitigate increased carbon costs is key priority to strengthening long-term resilience and returns.”

It added that its global business model “enables optimisation between markets” and has “increased operational flexibility and robustness” through its improvement programme.

This improvement plan includes “maintaining high production levels to ensure efficient asset utilisation, enabling reliable supply to a fertiliser market impacted by significant supply shocks.”

Yara also has the flexibility to source ammonia globally, allowing it to “optimise production if higher European gas prices reduce the profitability of ammonia production, as was the case in 2022”.

In recent years, Yara said it has demonstrated the resilience of its business model and is “uniquely positioned” to navigate volatility.

Future outlook

Yara highlighted that it is affected by “sanctions, shifting alliances, trade barriers, tariff changes, and complex logistics resulting from geopolitical tensions”.

However, it stated it did not experience operational disruptions from geopolitical situations with material impact on Yara’s consolidated results in the first quarter of 2026.

Looking ahead, Yara said: “While nitrogen markets remain distorted across regions, India and China continue to shape the global balance.”

It stated that Indian urea output was partly curtailed in March due to gas shortages, driving significant tender activity.

“Chinese exports have been restricted during the domestic season, but could ease in the second half of 2026, reducing pressure on global supply–demand,” it added.

As of March 2026, Yara’s trade payables to companies linked to Russian-sanctioned individuals amounted to $162 million.

These payables relate to “goods received prior to the imposition of sanctions,” Yara explained.

It said: “The timing of these cash outflows remains uncertain, as future payments will depend on developments in sanction regulations.”

Based on current forward markets for natural gas and assuming stable gas purchase volumes, Yara’s gas cost for the second and third quarter 2026 is estimated to be $150 million higher and $120 million higher than a year earlier.